Food packaging can significantly influence the quality and safety of the food product in question by providing a barrier to moisture and other environmental conditions that may result in contamination and/or spoilage.

The U.S. demand for pet food packaging is expected to rise 4.8 percent annually to $2.5 billion by 2018. Growth will be based on the use of higher value, more sophisticated packaging and continued strength in pet food shipments. The proliferation of premium pet food brands will also spur packaging demand growth, as higher value containers will be required to provide superior graphics, puncture resistance to reduce likelihood of contamination and barrier protection for these more expensive, higher-quality products.

While limited design flexibility and the inconvenience of opening cans have been the chief drawbacks of metal pet food containers, this segment is attempting to increase its competitiveness by emphasizing the safety of steel cans and their environmental friendliness due to their recyclability and use of recycled content. A much lower rate of product recalls for pet food exists for food packaged in metal cans than for that packaged in plastic alternatives, due to the tight seal and tamper evidence in cans.

According to our new study, Pet Food Packaging, demand for metal cans in pet food packaging is forecast to rise 2.7 percent annually to $650 million in 2018. Cans held 29 percent of the pet food packaging market in 2013. The percentage of overall can demand in pet food packaging will continue to decline due to supplantation by other packaging types, including retort pouches, tubs and cups, and chubs. Pouch demand in pet food packaging is forecast to rise 8.3 percent per annum to $540 million in 2018, the fastest pace of growth among pet food packaging types. For small packages of dry food, pouches will continue to supplant bags. For wet food, retort pouches will continue to gain acceptance as an alternative to metal cans, growing in popularity due to peelable lids that are easier to open and allow the consumer to avoid cuts from metal edges and especially in applications where strength and stiffness are not primary factors.

Can demand growth is forecast to be below that for the overall pet food packaging market, based on the maturity of this traditional packaging type and the lack of value-added features that would increase demand. Although other drawbacks like heavier weight and the need for opening devices on some cans do exist, an advantage does exist in that metal cans are the most recycled food or beverage container type.

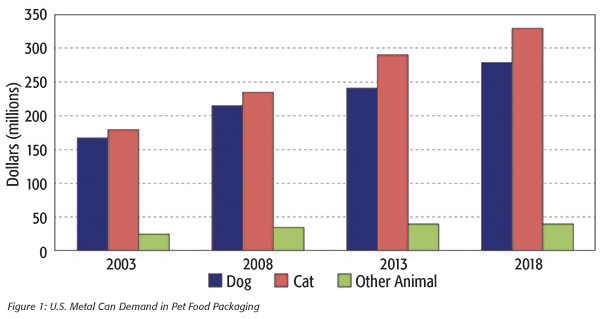

Other advantages include their low cost, long shelf life, durability and amenability to wet food products, ultimately reducing chance of contamination and spoilage. Additionally, the presence of easy opening ends will support continued opportunities. Fast-filling speeds and line efficiencies also support can use and make some manufacturers reluctant to shift production to plastic alternatives, which are slower to manufacture and involve added production costs (Figure 1).

Other advantages include their low cost, long shelf life, durability and amenability to wet food products, ultimately reducing chance of contamination and spoilage. Additionally, the presence of easy opening ends will support continued opportunities. Fast-filling speeds and line efficiencies also support can use and make some manufacturers reluctant to shift production to plastic alternatives, which are slower to manufacture and involve added production costs (Figure 1).

This study analyzed the $2 billion U.S. pet food packaging industry. It presents historical demand data for 2003, 2008 and 2013, and forecasts for 2018 and 2023 by application (e.g., dry food, wet food, pet treats, chilled and frozen), animal (e.g., dog food, cat food), type (e.g., bags, metal cans, pouches, folding cartons, plastic bottles and jars, tubs and cups) and material (paperboard, plastic, metal, wovens).

Joe Pryweller is an analyst for The Freedonia Group, an industry market research consultancy. For more information, please visit www.freedoniagroup.com.